0DTE Options: Opportunities and Risk

Introduction to 0DTE Options:

0DTE (Zero Days to Expiration) options have rapidly gained popularity among active traders, particularly in index options markets. As the name suggests, these are options contracts that expire on the same day they are traded. This ultra-short time horizon fundamentally changes the risk-reward profile compared to traditional options strategies and demands a precise, disciplined approach.

This blog post breaks down what 0DTE options are, why they attract traders, and — critically — the risks that often get underestimated.

What Are 0DTE Options?

0DTE options are standard options contracts that are traded on their expiration day. For example, if an index option expires on a Friday, any trade opened and closed on that same Friday would qualify as a 0DTE trade.

With the expansion of daily expirations on major indices like the S&P 500 (SPX) and Nasdaq-100 (NDX), traders now have near-constant access to 0DTE opportunities throughout the week. This shift has turned what was once a "Friday-only" event into a daily high-velocity market environment.

Unlike longer-dated contracts, these instruments settle to their final value by the market close of the same session. This eliminates "overnight risk"—the danger of a price gap occurring while the market is closed—allowing traders to express a pure view on intraday price action or specific economic catalysts like Fed announcements.

Key characteristics:

- 1. Extremely short lifespan (hours, not days).

- 2. Accelerated time decay (Theta).

- 3. Heightened sensitivity to price movement (Gamma).

- 4. Minimal Extrinsic Value near expiration.

Key Characteristics of 0DTE Options:

Understanding the structural properties of 0DTE options is essential before approaching them as a trading instrument. Unlike conventional options with days, weeks, or months of life remaining, 0DTE contracts operate under fundamentally compressed dynamics that affect every aspect of pricing and risk.

Extremely short lifespan — hours, not days. A 0DTE position opened at market open must be managed and closed within the same session. There is no opportunity to wait for conditions to improve overnight.

Accelerated Theta (time decay). Theta — the daily erosion of an option's extrinsic value — reaches its maximum rate on expiration day. An option that retains significant premium at 9:30am can be near worthless by 3:00pm even if the underlying barely moves. This is a powerful tailwind for sellers and a constant headwind for buyers.

Heightened Gamma sensitivity. Gamma measures how quickly Delta changes as the underlying moves. On expiration day, Gamma spikes dramatically, especially for at-the-money (ATM) strikes. A small move in the underlying can cause a large, rapid shift in the option's directional exposure — creating both opportunity and instability.

Minimal extrinsic value near expiration. By the final hours of trading, option premiums are composed almost entirely of intrinsic value (if in-the-money) or are approaching zero (if out-of-the-money). This means the margin for error on timing is razor thin.

The Daily Expiration Revolution:

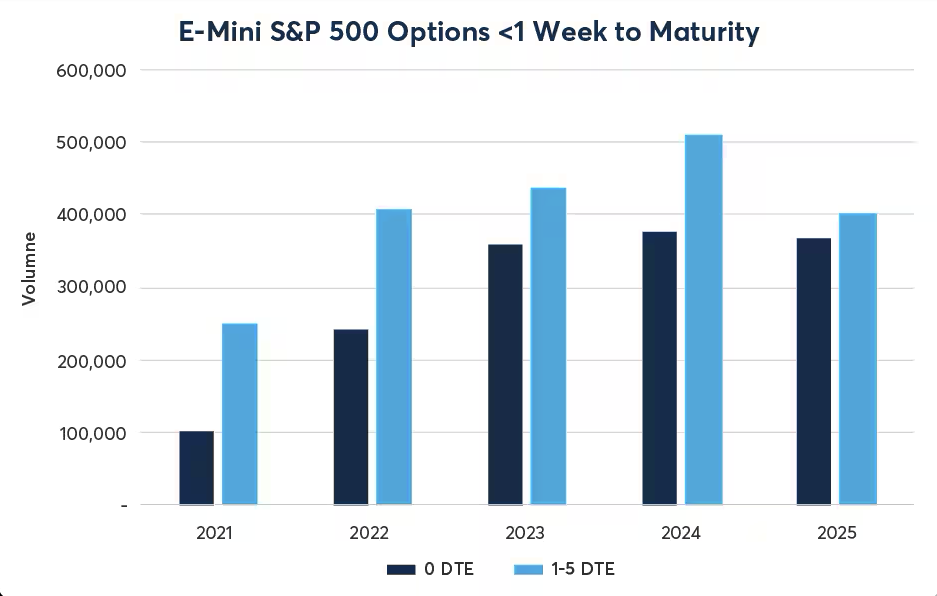

The proliferation of 0DTE trading has been driven by a structural change in how major index options are listed. Historically, index options expired only on a monthly or weekly basis. From 2022 onwards, the CBOE expanded SPX (S&P 500 index) options to expire every trading day of the week — Monday through Friday. Similar expansions followed for NDX (Nasdaq-100) and other major indices.

The result has been an extraordinary surge in volume. By 2023, 0DTE SPX options were accounting for over 40% of total SPX options volume on some trading days — a statistic that would have been unthinkable a decade earlier. Institutional market makers, prop trading firms, and increasingly retail traders now have constant, daily access to this instrument class.

For traders already using Black-Scholes-Merton pricing models, 0DTE options represent a specific and demanding use case. The BSM inputs — particularly implied volatility (σ) and time to expiration (T) — behave differently at this extreme time horizon. With T approaching zero, even small changes in σ produce significant swings in theoretical value, and the model's assumptions around constant volatility are most strained precisely when they matter most.

My 30-Bank BSM Pricing Calculator allows you to model 0DTE pricing directly — setting time to expiration in hours rather than days — giving you a quantitative framework to assess theoretical value and Greeks before you place a trade.

Why Traders Are Drawn to 0DTE

1. Rapid Profit Potential

Because these options are so close to expiry, even small moves in the underlying asset can produce significant percentage gains in a very short timeframe. A well-timed directional trade can deliver outsized returns within minutes — a 10% gain in a stock position that takes weeks might be replicated by a single correctly-timed 0DTE call in an hour.

This leverage effect is amplified by high Gamma. When the underlying moves sharply through your strike, Delta rapidly approaches 1.0 (for calls) or -1.0 (for puts), meaning the option begins to move nearly dollar-for-dollar with the underlying. For option buyers with modest capital outlay, this creates the potential for extraordinary percentage returns.

2. Theta Decay as a Weapon for Sellers

Option sellers are particularly attracted to 0DTE because time decay accelerates dramatically as expiration approaches. In a conventional option with 30 DTE, Theta might erode $5–$10 per day. In a 0DTE, the entire remaining extrinsic value — potentially the same $5–$10 — evaporates within a single session.

This creates a compelling proposition for premium sellers: collect a credit at open, watch time decay do the heavy lifting, and close or let expire by the end of the day. Provided the underlying stays within a defined range, the seller keeps the entire premium without waiting weeks for the position to play out.

The caveat is critical: while Theta is working in the seller's favour, Gamma is simultaneously working against them. A sudden directional move can destroy weeks of premium income in minutes. This asymmetry is the defining structural risk of 0DTE selling strategies.

3. Lower Nominal Capital Requirement

Compared to longer-dated options, 0DTE contracts are typically cheaper in absolute premium terms. A 30-day ATM option on a major index might carry $50–$80 of extrinsic value; the equivalent 0DTE may carry $10–$20. This lower price enables traders to take positions with less upfront capital outlay.

However, this is deeply misleading from a risk perspective. A cheaper option does not mean a safer trade. The percentage loss potential on a 0DTE — where a position can go from $15 to $0 in two hours — is extreme. Equating "cheap premium" with "low risk" is one of the most common and costly misconceptions among newer 0DTE traders.

4. No Overnight Risk

One of the most practically attractive features of 0DTE trading is the complete elimination of overnight gap risk. Positions are opened and closed within the same trading session. There is no exposure to after-hours earnings announcements, geopolitical events, central bank statements, or the myriad other catalysts that routinely gap markets open the following day.

For traders who have experienced being long options through an adverse overnight event — watching premium evaporate on the open — the intraday-only nature of 0DTE is genuinely appealing. It provides a clean, defined time horizon with no ambiguity about when the trade resolves.

5. Defined-Risk Structure

When traded as spreads (buying one strike, selling another), 0DTE options offer fully defined maximum risk and reward at the point of entry. Unlike futures or leveraged CFDs where losses can exceed initial margin, a vertical spread has a known worst-case outcome. This makes position sizing and risk management more tractable, even in a fast-moving environment.

6. Intraday Volatility Opportunities

Markets frequently exhibit pronounced intraday volatility patterns — particularly around scheduled economic data releases such as Non-Farm Payrolls, CPI, FOMC statements, and PMI readings. 0DTE options allow traders to take structured positions around these catalysts with a defined risk profile, rather than carrying naked directional exposure through news events.

Conversely, in the absence of catalysts, implied volatility on 0DTE options often compresses through the afternoon session, allowing premium sellers to benefit from both Theta and Vega compression simultaneously — a dual-factor edge not available on longer-dated contracts.

Understanding where implied volatility sits relative to recent realised volatility is therefore critical to 0DTE strategy selection. Our BSM calculators allow you to model both scenarios — testing theoretical option prices across different IV assumptions to identify whether current premiums represent fair value or opportunity.

The Core Risks of 0DTE Trading

While the upside is attractive, 0DTE options come with structural risks that are frequently underestimated — particularly by traders migrating from longer-dated options or directional equity strategies. These risks are not merely larger versions of standard options risks; they are qualitatively different due to time compression and Gamma dynamics.

1. Extreme Gamma Exposure — The Double-Edged Sword

As expiration approaches, Gamma increases sharply for near-the-money strikes, meaning the option's Delta can change dramatically with even small movements in the underlying. This creates a highly unstable profit and loss profile that can shift from profit to significant loss within minutes.

Consider a short ATM put sold for $8.00 when the underlying is at $5,000. With two hours to expiration, that option's Gamma might be 0.08 — meaning if the underlying drops just 10 points, Delta moves by 0.8. The option that appeared to be a safe income trade is suddenly deep in-the-money, and the premium received is now overwhelmed by intrinsic value.

For option sellers, high Gamma means positions can become intensely directional with alarming speed. For buyers, it means the window for a profitable exit can open and close within minutes. Hedging becomes increasingly difficult as Gamma rises, because the hedge ratio itself keeps changing rapidly.

2. Compressed Reaction Time

With only hours until expiration, the fundamental tools available to an options trader for position management are severely curtailed. Rolling a position to a further date is effectively unavailable on 0DTE. There is no time to "wait for the trade to recover." A conventional options trader with 30 DTE might comfortably watch a position move against them by $500, knowing they have weeks for conditions to revert. A 0DTE trader in the same situation has no such luxury.

Execution precision therefore becomes the strategy itself. Entry timing, strike selection, and exit rules must all be defined before entering the trade — not improvised in response to adverse movement.

3. The Illusion of High Win Rates

Many 0DTE premium-selling strategies — particularly short iron condors and credit spreads — can produce win rates of 80–90% in stable market conditions. What that narrative obscures is the risk-reward structure of the losing trades. A strategy that collects $200 in premium per trade and loses $1,800 on one in ten trades has an expected value of zero before costs — and negative after commissions and slippage.

The correct metric is not win rate — it is expected value per trade, which requires honest assessment of both the frequency and magnitude of losses. Many retail 0DTE strategies have not been tested through genuine volatility events such as flash crashes, surprise central bank interventions, or geopolitical shocks that can produce 2–3 standard deviation intraday moves.

4. Liquidity and Slippage

Major index 0DTE options are among the most liquid instruments in the world under normal conditions. However, liquidity is not constant throughout the session. In the first and last 30 minutes of the trading day, and around major economic data releases, bid-ask spreads can widen substantially — sometimes doubling or tripling relative to mid-session levels.

For a trader working with a $5.00 credit spread, a bid-ask spread that widens from $0.10 to $0.40 represents meaningful degradation in realised P&L. Over many trades, the cumulative impact of poor execution — entering wide markets, legging spreads incorrectly, or being forced to close at unfavourable prices — erodes an otherwise sound strategy.

Successful 0DTE traders treat execution quality as a core component of their edge. Limit orders, monitoring the NBBO, and avoiding trades during periods of acute spread widening are all essential disciplines.

5. Emotional and Cognitive Pressure

The psychological demands of 0DTE trading are substantially higher than for conventional strategies. The pace of P&L fluctuation is extreme — a position can move from $+800 to $-600 in the time it takes to read a news headline. Common failure modes include: holding losing positions beyond pre-set stop levels in the hope of recovery; closing winning positions prematurely out of fear; and overtrading following a loss in an attempt to recover capital within the same session.

Experienced traders structure their 0DTE approach with binary, pre-defined rules: defined entry criteria, maximum risk per trade, and mandatory exit levels — enforced without discretion. The psychological pressure to override these rules is precisely when they matter most.

6. Volatility Event Risk

Scheduled economic releases are predictable catalysts that 0DTE traders can plan around. Unscheduled events are not. A flash crash, a surprise geopolitical development, or an unexpected central bank statement can produce a 2–4 standard deviation intraday move in minutes. For a short options position, these tail events represent the maximum loss scenario arriving with no warning and no time to respond. Position sizing must account for this possibility on every single trade — not as a theoretical risk to be acknowledged and ignored, but as a probability to be quantified and respected.

Common 0DTE Strategies — with Real-World Examples

To move beyond theory, the following section breaks down realistic intraday 0DTE scenarios using concrete numbers, based on a highly liquid index (S&P 500-style pricing) and typical same-day expiry dynamics. Strike selection, entry timing, and scenario outcomes are all examined.

1. Credit Spreads — Bear Call Spread Example

Selling vertical spreads to capitalise on time decay while defining maximum risk is among the most widely used 0DTE approaches. The structure means the trader receives premium upfront and profits if the underlying remains below the short strike at expiration.

Market Context: Underlying index at $5,000 | Time: 10:15am | Bias: mildly bearish to neutral | Elevated but stable volatility.

Trade Setup:

Sell 5050 Call → Premium received: $8.00

Buy 5070 Call → Premium paid: $3.00

Net Credit: $5.00 ($500 per spread)

Max Profit: $500 | Max Loss: $1,500 | Break-even: 5,055

Scenario A — Price stays below 5,050: Both options expire worthless. Full $500 profit.

Scenario B — Price rises to 5,060: Approaching break-even. Small loss or scratch depending on exit timing.

Scenario C — Sharp move to 5,080: Spread fully in-the-money. Maximum loss: $1,500.

Key insight: Even a 1–2% intraday move can completely flip this trade from maximum profit to maximum loss due to Gamma acceleration. The 1:3 risk:reward ratio requires a win rate above 75% simply to break even — before costs.

2. Iron Condors — Range-Bound Example

The iron condor combines a bear call spread above with a bull put spread below, creating a defined range within which the trader profits. It is a volatility-selling strategy rather than a directional one — a bet that the underlying will remain within a corridor until expiration.

Market Context: Underlying at $5,000 | Time: 11:30am | Expected range: 4,950–5,050 | Volatility compressing.

Trade Setup:

Call side: Sell 5050 Call $7.00, Buy 5070 Call $2.50 → Credit: $4.50

Put side: Sell 4950 Put $6.50, Buy 4930 Put $2.00 → Credit: $4.50

Total Net Credit: $9.00 ($900 per condor)

Max Profit: $900 | Max Loss: $1,100 | Upper B/E: 5,059 | Lower B/E: 4,941

Scenario A — Closes at 5,000: All options expire worthless. Full $900 profit.

Scenario B — Moves to 5,060: Call spread partially in-the-money. Small loss or scratch depending on exit.

Scenario C — Breakout to 5,100: Call side fully in-the-money. Maximum loss: $1,100.

Key insight: The iron condor works well in low-volatility, range-bound sessions and can fail catastrophically during directional breakouts. Using a BSM calculator to assess whether the premium collected fairly compensates for the range offered provides a genuine analytical edge.

3. Directional Scalping — Long Call Example

Buying calls or puts to capture intraday momentum is the most straightforward 0DTE approach for directional traders. Simple in concept, demanding in execution — requiring precise entry timing, awareness of Theta drag, and the discipline to take profits quickly rather than allowing time decay to erode a winning position.

Market Context: Underlying at $5,000 | Time: 1:45pm | Catalyst: strong upward momentum / technical breakout.

Trade Setup: Buy 5000 Call (ATM) → Premium paid: $12.00 ($1,200 per contract)

Scenario A — Quick move to 5,020: Option rises to ~$22. Profit: $1,000 per contract (83% return in minutes).

Scenario B — Slow grind to 5,010: Theta erosion partially offsets the intrinsic gain. Option rises to ~$15. Profit: only $300.

Scenario C — No movement: Pure Theta decay. Option drops to $6 within 90 minutes. Loss: $600 — despite being directionally neutral.

Scenario D — Reversal to 4,985: Option collapses to ~$2. Loss: $1,000 — nearly the entire premium.

Key insight: The 0DTE directional buyer faces a dual adversary — Theta eroding the position continuously, and the need for both directional correctness and speed. Being right about direction but wrong about timing is still a losing trade. Many experienced traders enforce a strict maximum hold time of 15–30 minutes regardless of outcome.

4. Gamma Scalping — Advanced / Institutional Level

Gamma scalping involves buying a straddle to gain long Gamma exposure, then dynamically hedging the resulting Delta using the underlying asset. The goal is to profit from large intraday price swings — regardless of direction — by repeatedly adjusting the hedge as the underlying moves.

Market Context: Underlying at $5,000 | Time: 12:30pm | Expectation: elevated intraday volatility, no clear directional bias.

Trade Setup (Long Straddle):

Buy 5000 Call $10.00 + Buy 5000 Put $9.00

Total cost: $19.00 ($1,900 per straddle)

Initial position: near Delta-neutral, high Gamma, high Theta drag.

Hedging Sequence:

Move 1 — Underlying rises to 5,020: Call increases to $22, Put drops to $3. Total ~$25. Unrealised gain: $600. Trader sells the underlying to re-establish Delta-neutrality.

Move 2 — Underlying falls back to 4,990: Call drops to $6, Put rises to $14. Total ~$20. Trader buys back hedge at a lower price — locking in profit from the oscillation.

Through multiple hedging cycles, the trader extracts profit from each swing — profit that is not dependent on the final direction of the market, but on the magnitude and frequency of intraday moves.

Key insight: Gamma scalping is the most demanding 0DTE strategy — requiring real-time Delta monitoring, rapid execution, and a clear understanding of when Theta drag will overcome Gamma profits. It is effectively the preserve of institutional traders and well-capitalised professionals. It is included here to illustrate the full spectrum of 0DTE approaches, not as a recommendation for the majority of retail traders.

Risk Management Principles for 0DTE Trading

In a zero-time environment, risk management is not a supplementary consideration — it is the core of the strategy. The following principles reflect the minimum disciplines required to trade 0DTE options with any expectation of long-term profitability.

Conservative Position Sizing — Always

No single 0DTE trade should represent a meaningful percentage of trading capital. The structural possibility of a maximum-loss event on any given day means that position sizes must be calibrated to survive those events without material damage to the overall account. A common guideline among experienced 0DTE traders is to risk no more than 1–2% of total capital on any individual trade.

Define Risk Before Entry

Use spreads or predefined stop-loss levels to establish maximum loss before entering. For spread strategies, maximum loss is mechanically defined by spread width minus the premium collected. For directional long strategies, a stop-loss at 50–70% of premium paid is a common discipline — exiting the trade if the option loses more than half its value rather than watching it approach zero.

Avoid Correlated Overexposure

Trading multiple 0DTE positions simultaneously across correlated instruments — for example, a short call spread on SPX and a short call spread on NDX — does not provide diversification. These instruments move together during sharp market events, meaning the loss scenario is effectively doubled. True diversification in 0DTE requires uncorrelated underlyings or opposing directional structures.

Respect Volatility Events — or Avoid Them

Many experienced 0DTE traders apply a simple rule: no new positions within 30 minutes either side of a major scheduled data release, unless the strategy is specifically designed to exploit the volatility event. The price action around releases is structurally different from normal intraday conditions — spreads widen, Gamma spikes, and model-based pricing assumptions break down temporarily.

Have a Strict, Unconditional Exit Plan

Every 0DTE trade must have defined exit criteria established before entry: a profit target, a maximum loss level, and a time-based exit. Many experienced traders exit all positions by 3:30pm regardless of status, avoiding the extreme Gamma volatility of the final 30 minutes of the session. These rules must be followed without discretion — the psychological pressure to override them is precisely when they matter most.

Use BSM Pricing to Validate Your Entries

One of the most valuable applications of a Black-Scholes-Merton calculator in 0DTE trading is the pre-trade sanity check. Before entering any premium-selling strategy, calculating the theoretical fair value of the options involved — at different implied volatility assumptions — allows you to assess whether the premium collected adequately compensates for the theoretical risk. If the option appears overpriced relative to recent realised volatility, there is a structural edge in selling it.

My 30-Bank BSM Calculator allows you to run multiple scenarios simultaneously — comparing theoretical values across different strikes, DTE settings, and IV assumptions in a single view. For 0DTE traders, this kind of rapid multi-scenario analysis is a fundamental part of a disciplined pre-trade process.

Model the Final Hours of an Option's Life

On expiration day, options pricing is most sensitive to time. Setting your BSM calculator's time-to-expiration input to reflect hours remaining — rather than days — gives a realistic picture of how Theta and Gamma will interact as the session progresses. Watching how theoretical value changes between a 4-hour DTE and a 1-hour DTE for the same strike illustrates the velocity of time decay in concrete terms, and can sharpen your exit discipline considerably.

Who Should — and Should Not — Trade 0DTE Options?

0DTE options are not inherently unsuitable instruments — but they are specialised tools that carry structural risks inappropriate for all market participants. They are best suited to traders who already have a thorough grounding in options mechanics: understanding how Delta, Gamma, Theta, and Vega interact; being able to read an options chain; and having experience managing multi-leg positions under pressure.

Beyond technical knowledge, 0DTE trading demands a specific psychological profile: the ability to make rapid decisions under P&L pressure without emotional interference, and the discipline to follow a pre-defined rule set even when deviation feels compelling in the moment. Traders who find themselves adjusting their stop levels or "giving the trade more room" in real time are exhibiting the behaviours that 0DTE will punish most severely.

0DTE is potentially appropriate for: Experienced options traders with a clearly defined strategy, strong execution discipline, conservative position sizing, and a track record of managing multi-leg positions in volatile conditions. It may also suit traders who specifically want to avoid overnight risk and prefer the clean resolution of intraday-only exposure.

0DTE is not appropriate for: Options beginners who are still learning core mechanics. Traders who have not yet mastered risk management on longer-dated strategies. Anyone who finds themselves holding losing positions beyond pre-set stops on conventional trades. And anyone treating 0DTE as a lottery ticket rather than a structured, probabilistic trading instrument.

Conclusion: Precision Over Prediction

0DTE options represent one of the most demanding and fast-paced segments of modern options markets. They offer genuine opportunities — for premium sellers exploiting compressed Theta, for directional traders seeking leveraged intraday exposure, and for volatility traders profiting from intraday price oscillations — but the risks are structurally amplified by time compression and Gamma dynamics in ways that distinguish them from every other options instrument class.

The defining insight of 0DTE trading is that success is less about prediction than about precision, discipline, and risk control. A trader who is directionally correct 60% of the time but manages position size badly will lose. A trader who is right 50% of the time but has excellent risk management and exit discipline may be consistently profitable. The game is not just about getting the direction right — it is about surviving the sessions where you do not.

The Black-Scholes-Merton model remains the standard quantitative framework for understanding what an option is worth relative to its inputs. Using a BSM calculator to model 0DTE positions before placing them — testing how theoretical value changes across different volatility assumptions and time intervals — provides an analytical foundation that separates disciplined 0DTE traders from those relying on intuition alone.

If you are modelling 0DTE strategies in a multi-leg calculator, precision in inputs — particularly implied volatility and time-to-expiration expressed in hours — is critical to producing P&L projections that reflect realistic intraday dynamics rather than end-of-day theoretical values.

Key Technical Observations Across All 0DTE Strategies

Strike Selection Is Everything

In 0DTE trading, small differences in strike selection produce dramatically different outcomes. The difference between selling a strike 20 points out-of-the-money versus 40 points out-of-the-money changes the Delta exposure, Gamma risk, probability of profit, and premium collected in ways that compound rapidly as expiration approaches.

A strike that appears safely out-of-the-money at 10:00am may be at-the-money by 1:00pm following a 0.4% move in the underlying. The BSM model quantifies this through Delta — a strike with 0.20 Delta carries approximately a 20% probability of finishing in-the-money under the model's assumptions. Using this data systematically is materially better than selecting strikes by visual inspection of a chart alone.

Premium Is Compressed but Deceptive

The absolute dollar cost of a 0DTE option is low — but this does not mean the option is inexpensive in risk-adjusted terms. A $12 ATM option that can go to zero within 90 minutes represents a 100% loss of premium far more quickly than a $120 option with 30 days of life remaining. Options are cheap on expiration day because time is nearly gone and probability is efficiently priced — the market is not mispricing 0DTE premiums; it is correctly reflecting the compressed time horizon.

Speed Dominates Outcome

In a standard 30-DTE options trade, a 10-minute delay in execution is largely inconsequential. In a 0DTE trade, 10 minutes can represent the difference between a profitable exit and a losing close. This places a premium on platform reliability, order routing quality, and pre-defined limit order levels. Many experienced 0DTE traders have their strikes, quantities, and target prices calculated before the session begins — so that when a setup presents itself, execution is a matter of seconds rather than minutes of calculation under pressure.

The Hidden Asymmetry of Selling Strategies

Short premium 0DTE strategies have a characteristic P&L distribution that is fundamentally asymmetric: frequent small gains clustered around the credit received, and occasional large losses that can dwarf those gains. This asymmetry is not a flaw to be managed around — it is the structural nature of the instrument. The credit received is the compensation for accepting the tail risk of a sharp intraday move.

Without strict controls on position size and maximum loss per trade, the expected value of a short-premium 0DTE strategy can easily be negative even with a high win rate. Understanding this asymmetry — and quantifying it honestly using a BSM pricing tool to model worst-case scenarios — is the analytical foundation on which any viable 0DTE selling strategy must be built.

Don't Let Market Uncertainty Catch You Off Guard: Stop Guessing. Start Knowing.

The same Black-Scholes Calculator used by Hedge Funds and Market Makers — Simplified for Serious Retail Traders.

✓ Instant Option Pricing.

✓ See your Exact Profit & Loss Before You Trade.

✓ Real-Time Greeks: Delta, Gamma, Theta, Vega & Rho.

✓ Calculate Risk:Reward Scenarios in One Click.

✓ Professional Edge Without the Learning Curve.

Trade Like a Professional — Gain Confidence with Data-Driven Decisions to Maximise Profits and Minimise Risk.

Unlock the Full Potential of Your Options Trading. Click "Buy Now" and Download Your Option Pricing 30x Bank Calculator Today.

Best of Luck in Your Options Trading,

Ian,

B.Sc. Finance (Hons), UWIST, Wales.

Related Black-Scholes-Merton Options Calculators:

Black-Scholes-Merton 10x Leg Option P & L Master Strategiser

Black-Scholes-Merton Greeks Calculator with Single Option Pricer

Black-Scholes-Merton Options Pricing Calculators (30x Banks)

Black-Scholes-Merton Implied Volatility Calculators (10x Banks)