Rho Explained: The Change in An Options Price In Relation To

Changes in Interest Rates

What Are Option “Greeks?”

Greeks Overview:

While Vega tells you how much an Option's price changes with changes in the percentage level of Implied Volatility (I.V.), Rho tells you the sensitivity of an Options price in respect to changes in Interest Rates. Understanding Rho is important for managing risk during times of increased central bank interest rate policy activity, especially for traders holding long options or writing short premium strategies.

Option Greeks are mathematical measures that describe how different factors will affect the price of an Options contract. These factors include changes in the Underlying Asset's Price, Time to Expiry, Volatility, Interest Rates. The Greeks are essential for traders to understand the risks and potential rewards of options trading.

Rho Explained in Detail:

1. Rho (ν): Sensitivity to Interest Rates

What it Measures:

Rho (𝜌) measures the rate of change in an Option’s price with respect to a one percentage point change in Interest Rates (I.R.), all other factors remaining constant. It represents how much an Option’s total premium expands or contracts as interest rates change. Rho for Long Calls and Short Puts is always expressed as a positive number — both Long Calls and Short Puts gain value when I.R. rises. Both Short Calls and Long Puts lose value when interest rates rise. Therefore, Rho for Short Calls and Long Puts is always expressed as a negative number.

For Long Calls and Short Puts, Rho is positive (rising interest rates increase the Option’s value). For Short Calls and Long Puts, Rho is negative (rising interest rates decrease the Option’s value, or increase the cost to carry for the holder). Rho is greatest for deep In-The-Money (ITM) options and for options with longer time to expiration.

Rho’s formula is derived from the Black-Scholes-Merton model, reflecting the cost of carry for the underlying asset. Ranges: Expressed in currency units per 1% move in I.R. (e.g., +$0.05 means the Long Call or Short Put Option would gain $0.05 of value for every 1% increase in interest rates).

Why Rho is Important (See Charts):

1. Rho changes across different "Moneyness" (ITM / ATM / OTM) levels. ITM Options have the highest Rho because they have the highest correlation to the underlying stock’s price. Since interest rates affect the "cost of carry" for holding the stock, deep ITM options—which act most like the stock—have the greatest pricing impact at this level.

2. Rho increases as expiration approaches. Unlike Theta, which accelerates near expiry, Rho grows as an Option has more time on its contract. With more days remaining, the cumulative effect of interest rates over the life of the option is greater, so I.R. changes have a compounding effect on the option’s present value.

3. Rho's Positive or Negative sign is directly related to whether you are a buyer (Long) or seller (Short) of Options. Long Option holders benefit from rising IV (Vega works for them). Short Option sellers are hurt by rising IV (Vega works against them), which is the primary volatility risk in premium-selling strategies such as covered calls, cash-secured puts, iron condors, and credit spreads.

Overview of Rho for a Long Call:

- Long Calls: Rho measures how much an Option's price increases for every one percentage point rise in interest rates, all else being equal. If the premium of a Long Call is $3.00 today and Rho is +0.04, then a 1% rise in rates will cause the option to be worth approximately $3.04. Rho is typically quoted to 4 decimal places.

- For Long Calls, Rho is always Positive, meaning rising interest rates increase the Option's value, benefiting the buyer. A rise in rates inflates the premium — the Long Call holder can sell the Option for more than they paid as the "cost of carry" for the underlying asset increases.

- The Positive sign for Long Call Rho reflects the fact that the buyer benefits when rates rise because it becomes more attractive to hold the Option rather than the stock itself, which requires more capital or financing as interest costs grow.

- Positive Long Rho indicates that the Option premium expands when interest rates climb. This is especially impactful for long-dated Options like LEAPS, where the time value is significantly influenced by the prevailing risk-free interest rate.

- This creates a specific dynamic for Long Call buyers: a rising interest rate environment independently increases the Option's value via Rho — even if the underlying price does not move.

- Rho is highest in absolute terms when the Option is deep in-the-money (ITM) and decreases as the Option moves out-of-the-money (OTM). Longer-dated Options are far more sensitive to Rho than near-term contracts, which have very little interest rate risk.

- The goal for buying a Long Call Option remains to profit from upward moves, but a rising rate environment provides a small "tail-wind" for the position value. The maximum loss is still limited to the premium paid, regardless of interest rate fluctuations.

Overview of Rho for a Short Call:

- Short Calls: Rho measures how much an Option's price changes for every one percentage point move in interest rates. For the Short Call seller, rising rates work against them — the option they sold increases in value, meaning they would need to pay more to buy it back. Rho is typically quoted to 4 decimal places.

- For Short Calls, Rho is Negative, meaning rising interest rates work against the seller by increasing the cost to close the position. Every increase in interest rates adds to the seller's unrealised loss, all else being equal. A more detailed explanation follows further down on this page.

- The Negative sign for Short Call Rho reflects the fact that the seller collected a premium upfront but now faces a market where rising rates inflate the call's value above what they received, creating a potential loss if the position is covered.

- Negative Short Rho indicates that the Short Call position loses value (for the seller) as interest rates rise. While often small, this risk can independently push the Option's value higher, even without a move in the underlying stock price.

- This creates an adverse dynamic for Short Call sellers: a rise in interest rates can independently increase the cost to close the position. A sharp hike in rates without any underlying price movement can still result in a loss for the seller.

- Rho risk is highest for deep in-the-money (ITM) positions and longer-dated expirations. Near-dated at-the-money (ATM) or out-of-the-money (OTM) short calls are generally less sensitive to interest rate changes.

- The goal for Writing (selling) a Call Option is to collect premium and have the option expire worthless. However, sellers should monitor interest rate trends when holding long-term contracts, as rising rates increase their liability via Rho.

Interest Rates and Long and Short Call & Put Option Pricing

1. Effect of Interest Rates on Option Pricing:

How Interest Rates Impact Long and Short Call Option Pricing: Interest rates play a key role in the time value component of Options:

Higher interest rates increase the present value of holding cash compared to holding the underlying asset. This generally raises the value of Call options since Calls allow buying the asset later without tying up capital now. Lower or 0% interest rates reduce this advantage, diminishing the time value of the Call option.

For Puts, a higher interest rate generally reduces the value of the option because a higher interest rate would increase the present value of holding a position in the underlying asset. This can lower the attractiveness of owning a long Put option.

In the Black-Scholes Merton Model:

- Long Calls:

- Gain in value because of the time value of money. At higher interest rates, the future payment of the Strike price (for the underlying asset) is discounted more heavily, reducing its present value. This makes it financially advantageous to hold a Call option, as you can defer the cost of buying the asset while your capital earns interest elsewhere.

- Short Calls:

Become riskier as their liability grows with the higher time value for the buyer.

- Long Puts:

Lose value since deferring the sale of the underlying asset becomes less attractive when interest rates rise.

- Short Puts:

Benefit from reduced buyer demand as Long Puts become less valuable in a high-interest-rate environment.

2. The Effect of 0% Interest Rates.

When the interest rate is 0%, there is no discounting of the future payoff.

- Long Calls:

- Reduced Value: The deferred payment advantage disappears because there’s no opportunity cost to holding cash. With no interest rate advantage, Long Calls lose some appeal, as there’s no benefit from deferring payment for the underlying.

- Time Value Erosion: Time value decreases and the Option price is influenced more by intrinsic value and volatility.

- ITM behaviour: Deep ITM Calls approach parity with intrinsic value faster because there’s no time value benefit from interest rates.

- Short Calls:

- Lower Risk: With no interest premium factored into the time value, Short Calls are less risky for sellers.

- The absence of interest rates eliminates the deferred payment advantage for the buyer.

- The liability of the Short Call seller is limited to the intrinsic value and volatility of the option, making the position relatively less risky.

- Narrow Price Gap: The pricing difference between Long and Short Calls shrinks due to the absence of an interest-rate-driven premium.

- Long Puts:

- The absence of interest rates eliminates the deferred payment advantage for the buyer.

- Increased Value: At 0% interest, Long Puts become more valuable since there’s no opportunity cost of holding the underlying.

- There is no discounting of the Strike price, so the relationship between the Live Long Put price (LP @ Now) and the Expiry price (LP @ Expiry) is more straightforward. The price of the Long Put will reflect primarily the intrinsic value and time value without any impact from interest rates.

- Time Value Boost: Buyers benefit more from Puts when there’s no incentive to sell the underlying asset immediately.

- Short Puts:

- Without interest rates, the liability of the Short Put seller is based entirely on intrinsic value and time value, with no discounting of the Strike price. The pricing of Short Puts becomes more symmetrical to Long Puts.

- Higher Liability: Short Puts become riskier as Long Puts gain value in a low or 0% interest rate environment.

- The liability of the Short Call seller is limited to the intrinsic value and volatility of the option, making the position relatively less risky.

- Greater Exercise Probability: The lack of interest income increases the attractiveness of exercising the Put, especially if the underlying is OTM.

3. The Effect of Positive Interest Rates.

Higher interest rates increase the risk for Long Calls:

With a positive interest rate, buying the underlying asset now would mean losing the opportunity to earn interest on that money. A Call option avoids this opportunity cost, making it more valuable. The time value of the Call grows due to the ability to defer payment while the underlying asset might appreciate in value. This effect is more pronounced for long-dated Calls, where the deferred cost savings have more time to compound.

- Long Calls:

- Positive Impact: Higher interest rates increase the value of Long Calls due to the deferred payment advantage. Buyers avoid tying up capital by purchasing the option instead of the underlying.

- Time Value Growth: This is especially pronounced for longer-dated Calls, as the deferred cost savings grow over time.

Higher interest rates increase the risk for Short Calls:

- Short Calls:

- Higher Liability: Sellers face greater risk because the increased time value makes the option more attractive to buyers.

- ITM Impact: For ITM Short Calls, the higher interest rates magnify the risk, as the intrinsic value combines with increased time value.

Interest Rates and Long and Short Call & Put Option Pricing (Cont.)

Higher interest rates decrease the value of Long Puts:

When you have a positive interest rate, the future payoff of the Option (at expiry) is discounted more heavily. This reduces the present value of the Option. For a Put Option, the price is impacted by the discounting of the Strike price, which means that at a higher interest rate, the future payoff from exercising the Option (Strike price minus asset price) is worth less today.

The expiry line represents the theoretical value of the option at expiration, based on the intrinsic value at that time.

Positive interest rates result in the Put Option price becoming slightly cheaper when the interest rate increases. For Long Put pricing, this discounting effect from interest rates causes the dipping below the expiry price line at non-zero interest rates.

- Long Puts:

- Negative Impact: Long Puts lose value with higher interest rates. Selling the underlying asset now to earn interest becomes more appealing than deferring the sale via a Put.

- Weaker Demand: This reduces the attractiveness of Long Puts, especially OTM Puts, which rely heavily on time value.

Higher interest rates decrease the risk of Short Puts:

- Short Puts:

- Reduced Risk: Sellers benefit as Long Puts lose value, lowering the liability (with the objective of selling them at a high price and buying them back for less to close the contract).

- OTM Advantage: Short Puts are less likely to be exercised, and premiums collected become relatively safer.

4. Summary of Interest Rate Effects on Calls and Puts.

0% Interest Rates:

- Long Calls:

- Reduced Value: With no interest rate advantage, Long Calls lose some appeal, as there’s no benefit from deferring payment for the underlying.

- Time value diminishes, with prices driven more by intrinsic value and volatility. ITM behaviour: Deep ITM Calls approach parity with intrinsic value faster because there’s no time value benefit from interest rates.

- ITM behaviour: Deep ITM Calls approach parity with intrinsic value faster because there’s no time value benefit from interest rates.

- Short Calls:

- Lower Risk: With no interest premium factored into the time value, Short Calls are less risky for sellers.

- Narrow Price Gap: The pricing difference between Long and Short Calls shrinks due to the absence of an interest-rate-driven premium.

- Long Puts:

- No discounting effect, so the live price and expiry price are closely aligned.

- No dipping of the live price under the expiry line occurs, as the future value equals the present value which explains why the dip in the live long Put price disappears when interest rates are set to 0%.

- Increased Value: At 0% interest, Long Puts become more valuable since there’s no opportunity cost of holding the underlying.

- Time Value Boost: Buyers benefit more from Puts when there’s no incentive to sell the underlying asset immediately.

- Short Puts:

- Lower Risk: With no interest premium factored into the time value, Short Calls are less risky for sellers.

- Narrow Price Gap: The pricing difference between Long and Short Calls shrinks due to the absence of an interest-rate-driven premium.

Positive Interest Rates:

- Long Calls:

- Gain value from deferred payment advantage. Time value increases, making them more attractive for buyers.

- Short Calls:

- Become riskier as time value grows. Sellers face greater liabilities, especially with ITM options.

- Long Puts:

- Lose value since holding cash and earning interest becomes more attractive. OTM Long Puts are particularly affected as their time value diminishes.

- Short Puts:

- Benefit from reduced liability as Long Puts lose value. Safer to sell, particularly when underlying prices are stable or rising.

By analysing these effects, we can see how interest rates influence both Call and Put options, impacting strategies for buyers and sellers alike.

Conclusion:

The behaviour with the Put Price crossing below the Expiry Price could be due to the limitations of the Black-Scholes-Merton model in pricing DITM European Puts, where the time value (which the model calculates) may be misrepresented. This could explain why the model's results differ from what we'd expect if early exercise or arbitrage opportunities were factored in.

In short, this discrepancy is not only caused by interest rates as discussed above, but also likely caused by the inherent assumptions of the Black-Scholes-Merton model regarding early exercise and carrying costs, which don't fully match real-world market conditions, particularly for DITM options.

Loan Rate Debtor Perspective:

When a trader considers buying a Call Option, they are essentially choosing between buying the Option or borrowing money to purchase the Underlying Asset outright. Higher loan rates increase the cost of borrowing, making it more expensive to buy the Underlying Asset directly. This makes the Call Option relatively more attractive because:

- The Call Option allows the trader to gain exposure to the Underlying Asset without borrowing money.

- The trader avoids the high interest payments associated with borrowing at exponent loan rates.

- Therefore, higher loan rates increase the value of Long Calls because they make the alternative (borrowing to buy the underlying) more expensive.

For a trader selling (writing) a Call Option, higher loan rates increase the risk. If the Call is exercised, the seller may need to borrow money to deliver the Underlying Asset. Higher loan rates make this more expensive, increasing the potential loss for the Short Call seller. Thus, exponent loan rates increase the risk for Short Calls.

A Long Put gives the holder the right to sell the Underlying Asset at the Strike price. If loan rates are high, the trader might be motivated to sell the Underlying Asset immediately and invest the proceeds at a high interest rate, rather than holding a Put Option. This reduces the value of the Long Put because:

- The opportunity cost of holding the Put (instead of selling the underlying and earning interest) increases.

- Therefore, higher loan rates decrease the value of the Long Put.

For a Short Put seller, higher loan rates reduce the risk. If the Put is exercised, the seller must buy the Underlying Asset, which may require borrowing money. However, if loan rates are high, the likelihood of the Put being exercised decreases because the buyer (Long Put holder) would prefer to sell the Underlying Asset immediately and earn interest, rather than exercise the Put. Thus, exponent loan rates decrease the risk for Short Puts.

Summary of Exponent Loan Rate Effects (Debtor Perspective):

Higher interest rates decrease the value of Long Puts:

- Effect: Value increases with higher loan rates.

- Reason: Borrowing to buy the underlying becomes more expensive, making the Call Option more attractive.

- Effect: Risk increases with higher loan rates.

- Reason: Delivering the underlying upon exercise may require expensive borrowing.

- Effect: Value decreases with higher loan rates.

- Reason: The opportunity cost of holding the Put (instead of selling the underlying and earning interest) increases.

- Effect: Risk decreases with higher loan rates.

- Reason: The likelihood of exercise decreases as the Long Put holder prefers to sell the underlying and earn interest.

Key Insight:

From a debtor perspective, exponent loan rates affect Options pricing by changing the cost of borrowing and the opportunity cost of holding positions. This is because higher loan rates make borrowing more expensive, which influences the relative attractiveness of Options versus direct positions in the Underlying Asset.

Examples:

Real-World Context: Imagine you're an investor in early 2026, analysing Microsoft Call options during a period of changing interest rates.

Scenario A: Low Interest Rate Environment (2-3%):

Call Option Details:

- Microsoft Stock Price: $350

- Strike Price: $360

- Implied Volatility 30%

- Days to Expiry (DTE) Expiration: 3 months (90 days = 24.66%)

- Call Option Premium at 3% interest rate: $17.52

Scenario B: High Interest Rate Environment (6-7%):

Same Microsoft Stock BSM Inputs

Option Premium at 7% interest rate: $19.03

Practical Explanation:

The $1.51 premium increase reflects the higher opportunity cost. At 7% interest rates, the time value of money becomes more significant. The option becomes more expensive because:

- The present value of the Strike price decreases.

- Alternative risk-free investments become more attractive.

- The cost of capital increases.

Consider how a bank's savings account rate of 7% impacts your decision to buy this option versus simply depositing money.

Scenario 2: Airline Industry - Delta Airlines (DAL) Put OptionReal-World Scenario: You're hedging risk in the volatile airline industry during 2026 by buying a Put.

Scenario A: 0% Interest Rate:

Put Option Details:

- Delta Airlines Price: $40

- Strike Price: $35

- Implied Volatility 20%

- DTE Expiration: 6 months (180 days = 49.32%)

- Put Option Premium at 0% interest rate: $0.48

- Stock Price: $40

- Break-even Point: $34.52

Scenario B: Rising Interest Rate Environment:

- Same Stock Parameters

- Option Premium: $1.75

- Break-even Point: $33.25

Practical Implications:

The lower premium in the high-interest-rate scenario demonstrates:

- Higher rates increase the opportunity cost of holding options, increasing the opportunity cost of holding protective Puts.

- Decreased Put option value.

- Investors may seek alternative risk management strategies as alternative investment strategies become more attractive.

Investment Insight: As interest rates rise, the cost of insurance (Put options) becomes relatively less attractive.

Examples: (cont.)

Scenario 3: Emerging Market Currency Option - Indian Rupee (INR)Real-World Context: Multinational corporation hedging currency risk between USD and INR.

Scenario A: Low Interest Rate Differential:

Call Option Details:

- Current Exchange Rate: 83 INR/USD

- Strike Rate: 85 INR/USD

- DTE Expiration: 1 year

- Option Premium at 3% interest rate differential: $1.91

Scenario B: High Interest Rate Differential:

Same Exchange Rate Parameters

Option Premium at 7% interest rate differential: $0.15 ($4.13)

Practical Analysis:

The premium reduction illustrates:

- Higher interest rates increase option value because the present value of the Strike price (the amount to be paid at expiration) is discounted more heavily.

- Currency option pricing becomes more complex with interest rate changes.

- Investors must constantly reassess hedging strategies.

Example: Investment Scenario integrating multiple factors:

Investment Goal: Balanced portfolio protection

Market Condition: Interest rates rising from 3% to 7%

Option Strategy Adjustments:

- Reduce long Put positions.

- Carefully select Call options with longer expiration.

- Increase focus on covered Call strategies.

- Consider converting some option positions to direct stock investments.

Key Takeaways:

- Interest rates are not static; they're dynamic market signals.

- Option pricing is a sophisticated interplay of multiple factors.

- Successful investors continuously adapt their strategies.

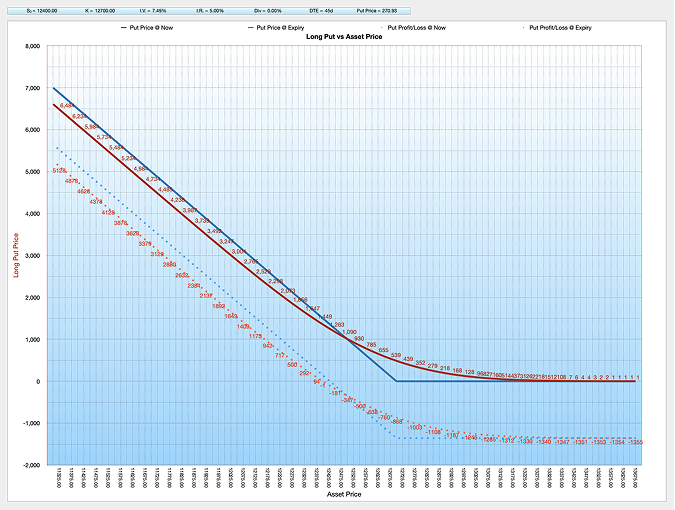

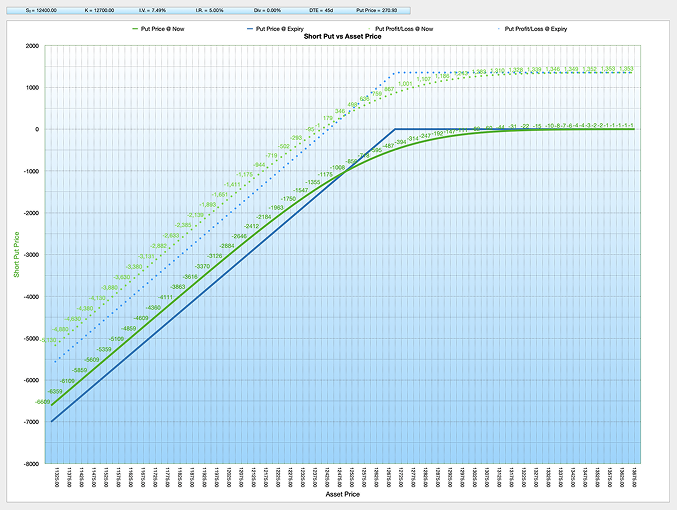

Long and Short Put Option Prices Crossing the Expiry Price

Recapping briefly on Option types from my Types of Option page, it becomes apparent from the Long and Short Put charts, reproduced below, that there is a crossing over or dipping under and over of the Live @Now Put price line and the @Expiry price line.

Long Put Option: Long Put Options are for buyers who are bearish (expecting the price to go down) on the asset.

Causes of Put Option Prices Dipping Under and Over the Expiry Price

What factors could be causing this pricing behaviour? Below I cover the factors that cause this, in what at first I thought was a mistake in my calculations when creating the Single Option Pricer with Greek Charts.. Images below.

Short Put Option: Short Put Options are for sellers who are bullish (expecting the price to go up) on the asset.

Why the Long & Short Put @Now (live) Curved lines Dip

Under and Over the @Expiry Price line

European Calls may be worth less than their intrinsic value. Intrinsic Value is the difference between the Strike price and the Underlying Asset Price.

The Black-Scholes-Merton model can only be used to price European options accurately, although for non-dividend paying stocks the American Call price is exactly the same as the European call price. The Black-Scholes-Merton model only takes into account the position at expiration, (whereas, eg, a Binomial Option Pricing model can calculate prices upon and including up to expiration).

With Puts and even on non-dividend paying stocks the fair value of a DITM (Deep-in-the-Money) European Put can be less than its intrinsic value due to:

Interest rates, the carrying costs on the positions (which arbitrageurs undertaking conversions would have to carry through to expiration). American Puts, on the other hand, cannot trade at a discount to parity as they would be quickly exercised by arbitrageurs.

Root causes of the time value discrepancies and the crossing behaviour between the Put Price @ Now and Put @Expiry Price on Put charts:

Key Points:

1. European Calls & Puts and Interest Rates:

For European Puts, the fair value can be less than its intrinsic value due to interest rates. Rates play a key role in determining the present value of the future payoff (Strike minus Stock Price at expiration).

If the interest rate is positive, there's a time value of money effect, meaning that the future cash flows (payoff at expiration) are discounted back to the present. This discounting can cause the Put price to be less than its intrinsic value today, especially for DITM Puts.

A similar relationship occurs for Calls in terms of the opportunity cost for holding cash, and how that affects the valuation of the option in real-world market contexts where interest rates influence decision-making. Investors have to compare the option's pricing to alternatives such as holding a bond at a high or low interest rate. These carrying costs are not factored into the Black-Scholes-Merton model. These carrying costs are not factored into the model, which focuses only on the intrinsic value (the difference between the Strike price and the Underlying Asset Price) at expiration and doesn't account for any intermediate steps or actions that might affect the option's price prior to expiry.

2. European Puts and Carrying Costs

Carrying costs include the costs associated with holding the underlying asset or a short position in an option until expiration, which would influence the market value of the option. In DITM (deep in-the-money) Put options, arbitrageurs might find it profitable to exercise early, thereby driving the price of American Puts higher than their theoretical value from the Black-Scholes-Merton model.

These carrying costs are not factored into the model, which focuses only on the intrinsic value (the difference between the Strike price and the Underlying Asset Price) at expiration and doesn't account for any intermediate steps or actions that might affect the option's price prior to expiry.

3. American Puts and Early Exercise

The Black-Scholes-Merton model assumes European-style options, meaning that it doesn't account for the possibility of early exercise.

In contrast, American Puts can always be exercised early. This gives them an additional premium, which the Black-Scholes-Merton model does not capture because it only applies to European-style options (which cannot be exercised early).

Like American style options, this could lead to underpricing of European Put options at certain points, especially if the option is DITM.

It in part explains why, at some asset prices, the calculated Long Put @Now price is lower than the @Expiry price, since the model might not factor in the carrying costs or other market conditions, such as dividends or arbitrage opportunities.

4. European Puts (Black-Scholes-Merton)

The expiry price represents the theoretical price at expiration, while the current price, the Long Put @Now price, incorporates market expectations and potential early exercise which isn't captured by Black-Scholes for European Puts.

Because the Black-Scholes-Merton model assumes European-style options, it doesn't account for the possibility of early exercise like American style options. This can lead to the underpricing of Put options at certain points, especially if the option is DITM and the market anticipates that the option could be exercised early (which wouldn't be accounted for in the Black-Scholes-Merton model).

It in part explains why, at some asset prices, the calculated Long Put @Now price is lower than the @Expiry price, since the model might not factor in the carrying costs or other market conditions, such as dividends or arbitrage opportunities.

The rest of this page will cover Interest Rates specifically:

Rho Impact — Monetary Effect of a +1% Interest Rate Rise:

Long Positions: Profit/Loss from +1% Rate Rise

| Position | Moneyness | Initial Premium | Rho | New Premium (+1% Rate) | P&L Impact |

|---|---|---|---|---|---|

| Long Call | ITM | $5.80 | +0.12 | $5.92 | +$0.12 Profit |

| Long Call | ATM | $3.00 | +0.06 | $3.06 | +$0.06 Profit |

| Long Call | OTM | $1.20 | +0.03 | $1.23 | +$0.03 Profit |

| Long Put | ITM | $5.50 | -0.10 | $5.40 | -$0.10 Loss |

| Long Put | ATM | $2.80 | -0.05 | $2.75 | -$0.05 Loss |

| Long Put | OTM | $1.10 | -0.02 | $1.08 | -$0.02 Loss |

Note: Long Calls benefit from rising rates (+ Rho) as the "cost of carry" makes the option more attractive than buying stock. Long Puts lose value (- Rho) as rates rise. Rho is typically more significant for longer-dated options (LEAPS).

Short Positions: Profit/Loss from +1% Rate Rise

| Position | Moneyness | Premium Collected | Rho | Buy Back Cost (+1% Rate) | P&L Impact |

|---|---|---|---|---|---|

| Short Call | ITM | $5.80 | +0.12 | $5.92 | -$0.12 Loss |

| Short Call | ATM | $3.00 | +0.06 | $3.06 | -$0.06 Loss |

| Short Call | OTM | $1.20 | +0.03 | $1.23 | -$0.03 Loss |

| Short Put | ITM | $5.50 | -0.10 | $5.40 | +$0.10 Profit |

| Short Put | ATM | $2.80 | -0.05 | $2.75 | +$0.05 Profit |

| Short Put | OTM | $1.10 | -0.02 | $1.08 | +$0.02 Profit |

Note: For sellers, rising rates are disadvantageous for Short Calls (increasing their value/cost to close) but advantageous for Short Puts (decreasing their value/cost to close). Rho impact is generally the least influential Greek for short-term trades.

Master Interest Rate Effects with the Single Option Pricer and Greek Charts Calculator.

Understand how Interest Rates impact your Option strategies. Model different Rate scenarios and see real-time pricing changes.

Trade Like a Professional — Gain Confidence with Data-Driven Decisions to Maximise Profits and Minimise Risk.

Click the "Buy Now" Button and Download the BSM Option Pricer with Greek Charts Today. Available in both Excel and Apple Numbers:

Best of Luck in Your Options Trading,

Ian,

B.Sc. Finance (Hons), UWIST, Wales.

Related Black-Scholes-Merton Options Calculators:

Black-Scholes-Merton 10x Leg Option P & L Master Strategiser

Black-Scholes-Merton Greeks Calculator with Single Option Pricer

Black-Scholes-Merton Options Pricing Calculators (30x Banks)

Black-Scholes-Merton Implied Volatility Calculators (10x Banks)